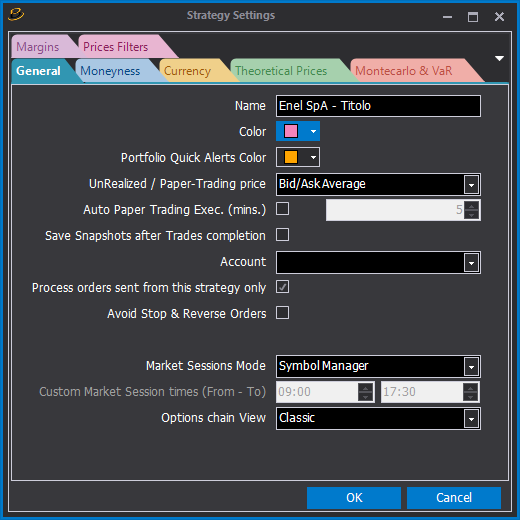

Options Strategy – Strategy Settings

- Name: name of the strategy;

- Color: reference color of the strategy;

- Portfolio Quick Alerts Color: color used to identify the strategy in the Portfolio when there are Quick Alerts;

- UnRealized / Paper-Trading price: prices on which the strategy Un-Realized is calculated and paper-trading orders are filled;

- Auto Paper Trading Exec .: if the box is checked, non-completed orders (in basket) will be automatically finalized in paper-trading, after the specified interval, expressed in minutes;

- Save Snapshot after trader completation: saves the properties of the strategy when a trade is made (useful for having historicity);

- Account: identifies the account to which the strategy is associated (the one with which it was built). If your account has multiple accounts, you can choose the desired account which will be the one where the orders will be sent;

- Process orders from this strategy only: if the box is checked, only real market orders made by the strategy itself are recorded within the strategy and not, for example, by trading systems active on the same assets in beeTrader;

- Avoid Stop & Revers Orders: the result of the trade is the same but I pay less commissions on We BanK using the “intra” function;

- Market Session Mode: select the trading time mode;

- Custom Market Session times (From – To): allows to customize the market session times, if Market Session Mode is set to Custom;

- Options Chain View: select the view mode. Info at this link.

-

Alternative Underlying: another underlying may be used, among those included in the Strategy, for example a future;

-

Put / Call Parity: for each expiry the value of the underlying is calculated through the Put / Call Parity . It is necessary to set only the necessary deadlines and the Risk Free Rate;

-

Underlying with Dividends: the price of the underlying is adjusted based on dividends entered by the user in Symbol Manager. It is also possible to enter the dividends using the appropriate button on the window;

-

Underlying without Dividends: the underlying is used ignoring any dividends entered.

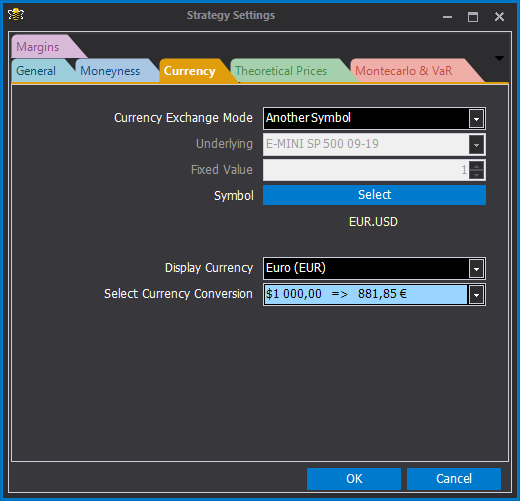

- Currency Exchange Mode: from the menu choose the currency conversion mode between None, Underlying, Fixed, Another Symbol;

- Underlying: in this case the strategy uses the underlying asset to set the currency exchange rate. Use this mode if the trading account is the euro currency and the EUR-USD future is translated;

- Fixed Value: in this case it is possible to set the exchange rate by hand. Please note that this value will remain constant until it is manually adjusted;

- Symbol: in this case it is possible to choose any asset, among those available, which will act as an exchange rate. Use this mode by choosing the EUR-USD future if the trading account is in euros and using instruments valued in dollars, such as for example AUD-USD futures. future MINI SP 500, future MINI NASDAQ or US equities.

- Currecy display: the currency that will be displayed;

- Select Currency Conversion: choose the conversion rate to set.

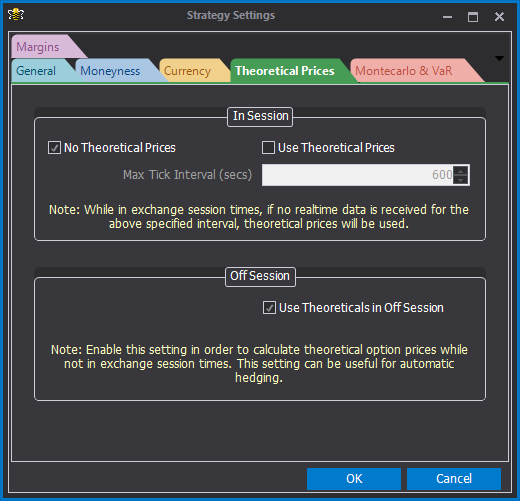

In this section it is possible to set the use of the theoretical options prices. The theoretical prices are calculated by beeTrader based on acquired and processed volatility curves, it is recommended to read the appropriate section of the manual to this link .

In Session: choose whether to use the theoretical prices and eventually set after how many seconds from the last realtime update the theoretical price must take over;

Off Session: set whether to use the theoretical prices outside the market session of the underlying set in Symbol Manager .

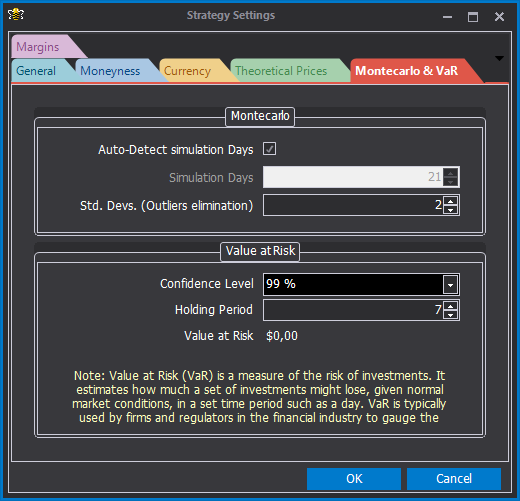

From this section it is possible to set the parameters for calculating the Monte Carlo simulation and the Value At Risk. The settings relating to Monte Carlo will be applied both for the calculations and for the payoff.

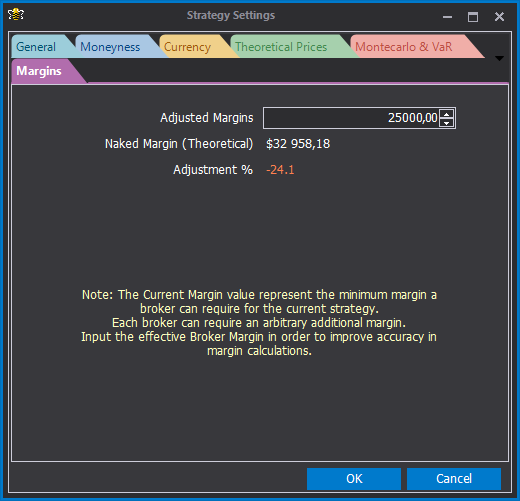

In this section it is possible to align the margin calculated by beeTrader with that actually requested by the broker for its own strategy. The margin calculated by beeTrader is the margin required by the cash desk and compensation. At this margin each broker applies an additional percentage that is requested to the user. Once the strategy is saved the value imputed by the user is also transferred to the Portfolio .

Example:

the strategy is put on the market and the margin deviation occurs, we assume it is 350%, at this point we know that the difference between the broker’s margin and the theoretical margin is 350%, therefore it is adjusted and this remains for the rest of the strategy.

The Naked Margin is used because the margin with risk-defined strategies coincides with the maximum risk and it is not necessary to calculate it, so you know, in the event of a spread, if you close the bought part first what will be the required margin. </ b>